❖본 조사 자료의 견적의뢰 / 샘플 / 구입 / 질문 양식❖

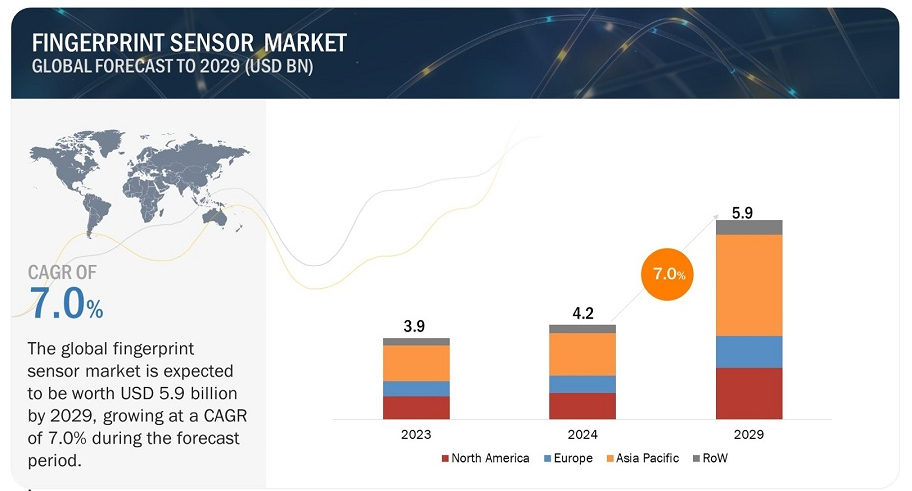

글로벌 지문 센서 시장은 2024년 42억 달러에서 2029년까지 59억 달러에 이를 것으로 예상되며, 이 기간 동안 연평균 성장률(CAGR)은 7.0%에 이를 것으로 보입니다. 생체 인식 기술을 기반으로 한 출석 기록 시스템의 도입은 직원의 출석 및 시간을 추적하는 데 도움을 주며, 이는 시장 성장의 주요 요인으로 작용하고 있습니다. 지문 기술 기반 시스템은 사용자 친화적이며 설치가 용이하여 관리자가 직원 데이터를 추적하고 분석하는 데 유리합니다. 이러한 시스템의 주요 장점 중 하나는 직원들이 서로 대신 출석하는 것을 방지할 수 있다는 점입니다. 이는 기존의 시간 기록기, 서명 시트 및 ID 카드 스와이프와 같은 방법에서 흔히 발생하는 문제입니다. 지문 센서는 출석 사기를 크게 줄이는 데 기여하고 있습니다. 본 보고서의 목적은 기술, 센서 기술, 유형, 최종 사용 애플리케이션 및 지역에 따라 지문 센서 시장 점유율을 정의하고 설명하며 예측하는 것입니다. 지문 센서 시장의 동력으로는 신원 위협의 증가가 있으며, 이는 지문 기술의 출현을 촉진하고 있습니다. 신원 도용은 개인의 개인 정보나 재정 정보를 불법적으로 획득하여 사기를 저지르는 행위를 말합니다. 최근 신원 위협이 증가하고 있으며, Aite Group에 따르면 2022년 25세에서 34세 사이의 소비자 중 33%가 신원 도용을 경험했습니다. 반면, 미국 연방거래위원회(FTC)가 유지하는 소비자 센티넬 네트워크에 따르면 2022년 신원 도용 사건이 2021년보다 23% 감소했습니다. 제한 요인으로는 얼굴 및 홍채 스캔과 같은 대체 기술의 채택 증가가 있습니다. 이러한 대체 기술은 지문 인식의 지배력을 위협하고 있으며, 얼굴 인식 시스템은 원격 인식에 적합합니다. 또한, 홍채 스캔은 고유한 홍채 특성을 캡처하여 보안을 강화합니다. 예를 들어, JetBlue는 전통적인 탑승권 대신 얼굴 인식 기술을 탐색하고 있으며, 은행 및 금융 부문에서는 고객의 신원을 확인하기 위해 얼굴 인식 기술을 활용하고 있습니다. 기회로는 IoT 기반 생체 인식 기술의 채택 증가가 있습니다. IoT의 발전은 스마트 객체를 인터넷에 연결하여 데이터 교환을 원활하게 하고 있습니다. 그러나 연결된 장치의 수가 증가함에 따라 정보 유출이나 침해의 위험이 커지고 있습니다. 생체 인식 기술은 IoT 네트워크 내에서 안전한 연결을 보장하는 솔루션을 제공합니다. 현재 비밀번호나 PIN으로 장치와 거래 프로세스를 보호하고 있지만, 보안이 취약한 연결은 악성 소프트웨어 공격에 노출될 수 있습니다. 지문 솔루션과 같은 생체 인식 시스템을 구현하면 장치 보안을 강화할 수 있습니다. 도전 과제로는 센서 성능의 한계가 있습니다. 센서 성능의 제한은 지문 센서 시장의 주요 장애물로 작용하며, 다양한 산업에서의 광범위한 채택과 효과성에 영향을 미칩니다. 환경 조건이나 사용자 생리학적 요인에 의해 성능이 저하될 수 있으며, 예를 들어 건조하거나 땀에 젖은 손가락은 센서가 명확하고 정확한 지문 이미지를 캡처하는 데 방해가 될 수 있습니다. 이는 인식 실패로 이어져 사용자에게 불편을 초래할 수 있습니다. |

The global fingerprint sensor market size is projected to grow from USD 4.2 billion in 2024 and is expected to reach USD 5.9 billion by 2029, growing at a CAGR of 7.0% from 2024 to 2029. Implementing biometric technology-based time and attendance registering systems has simplified tracking employees’ time and attendance and is driving the market. Fingerprint technology-based systems are user-friendly and easy to install, aiding management in tracking and analyzing employee data. One of their main advantages is preventing employees from logging in for one another, a common issue with older methods like time clocks, sign-in sheets, and ID card swiping. Fingerprint sensors have significantly reduced attendance fraud.

The objective of the report is to define, describe, and forecast the fingerprint sensor market share based on technology, sensor technology, type, end-use application, and region.

Fingerprint Sensor Market

Fingerprint Sensor Market

Fingerprint Sensor Market Forecast to 2029

To know about the assumptions considered for the study, Request for Free Sample Report

Fingerprint Sensor Market Dynamics

Drivers: Rise in number of identity threats leading to emergence of fingerprint technologies

Identity theft refers to the illegal acquisition of an individual’s personal or financial details to perpetrate fraud, including unauthorized transactions. It occurs through various methods and inflicts harm on victims’ credit, finances, and reputation. Recently, there has been an increase in identity threats. According to the Aite Group, 33% of consumers between the ages of 25 to 34 years old experienced identity theft in 2022. On the other hand, according to the Consumer Sentinel Network, maintained by the Federal Trade Commission (FTC), there was a 23% decrease in identity theft in 2022 from 2021. In 2022, 1,108,609 reports were filed for identity theft, down from 1,434,693 in 2021.

Numerous identity theft protection services aid individuals in preventing and mitigating the repercussions of identity theft. These services offer guidance on safeguarding personal information, monitor public and private records such as credit reports for suspicious activity, and aid victims in resolving identity theft issues. Additionally, government agencies and nonprofit organizations offer similar assistance through websites equipped with tools and information to prevent, address, and report identity theft incidents. Similarly, financial institutions and government agencies utilize fingerprints and other biometric technologies to enhance identity verification and protect individuals from identity theft.

Restraint: Increased adoption of substitute technologies, such as face and iris scanning

The rise in substitute technologies such as facial and iris scanning challenges the dominance of fingerprint recognition, the most popular form of biometric security. While fingerprint recognition is well-established, other biometric parameters like iris/retina, voice, pulse, DNA, and vein offer enhanced security levels. Facial recognition and iris scanning are increasingly favored and may eventually replace fingerprint sensing. Facial recognition systems analyze facial features for identification, making them suitable for remote recognition. Similarly, iris scanning captures unique iris characteristics, which are encrypted for security. Iris scanning, particularly using infrared light, is recognized for its high security standards. For instance, JetBlue is exploring the use of facial recognition technology as an alternative to traditional boarding passes for authentication. Meanwhile, in sectors like banking and finance where security is of utmost importance, institutions such as Bank of America, HSBC, Chase, and Apple’s FaceID are leveraging facial recognition technology to verify customers’ identities, access mobile banking applications, and execute transactions securely.

Opportunity: Increased adoption of IoT-based biometric technology

The advent of IoT has revolutionized automation systems by connecting smart objects to the internet, facilitating seamless data exchange. However, the increasing number of connected devices heightens the risk of information loss or breaches. Biometrics offers a solution for ensuring secure connections within the IoT network, protecting against fraud and theft. Currently, passwords or PINs safeguard devices and transaction processes, but unsecured connections are vulnerable to malware attacks. Implementing biometric identification systems, such as fingerprint solutions, enhances device security.

Biometric security measures can be integrated at different points in the IoT data pathway, from device authentication using fingerprint sensors to individual identity verification via smartcards. These security measures ensure the smooth flow of data between points while safeguarding data integrity. Continuous technological advancements are expected to further enhance fingerprint technology, given its widespread deployment across various devices.

Challenge: Sensor performance limitations

Sensor performance limitations represent a significant hurdle in the fingerprint sensor market size , impacting the broader adoption and effectiveness of this technology across various industries. It can be hampered by various factors, including environmental conditions and user physiology. For instance, dry, sweaty, or dirty fingers can impede the sensor’s ability to capture a clear and accurate fingerprint image. This can lead to failed recognition attempts, frustration for users, and ultimately, a weakened security posture. Additionally, certain professions or activities can lead to damaged or worn fingerprints, further reducing sensor effectiveness.

Fingerprint Sensor Map/Ecosystem:

Fingerprint Sensor Market by Ecosystem

Market for area & touch sensor segment is expected to witness higher CAGR during the forecast period.

An area or touch sensor is a type of sensor that simply requires users to press their finger against a designated area, often situated beneath the Home button, as seen in devices like the iPhone. The differentiation between touch and area sensors lies not in technology but in their intended applications. Touch sensors activate upon physical contact with an object or individual and are more sensitive compared to traditional buttons or manual controls.

Market for consumer electronics segment in the end-use application is expected to witness fastest growth in the fingerprint sensor market during the forecast period.

The fingerprint sensor market share in consumer electronics is experiencing exponential growth, fueled by increasing demand for secure authentication solutions in smartphones, tablets, laptops, and wearable devices. These sensors are utilized for unlocking devices, authorizing payments, and securing personal data, enhancing user convenience and data security. As consumers become more conscious of privacy and security concerns, the adoption of fingerprint sensors is expected to surge further.

Optical segment in the technology of fingerprint sensor market is expected to hold the second largest market share by 2029.

Optical sensors function by utilizing light and converting it into electrical signals to create fingerprint images. These sensors employ optical lenses, such as charge-coupled devices (CCD) and complementary metal-oxide-semiconductor (CMOS), along with light-emitting diodes (LEDs) for illumination. Using a light-emitting phosphor layer, the technology captures fingerprints through total internal reflection by illuminating the surface. The resulting image is then captured and stored.

Fingerprint sensor market in the Asia Pacific is estimated to grow at the fastest rate during the forecast period.

Asia Pacific accounted for the largest share of the overall fingerprint sensor market in terms of value in 2023 and is also expected to witness highest growth during the forecast period. The region’s large population is driving the market growth and the increasing demand for secure authentication solutions, causing the market to soar.Fuelled by the widespread adoption of smartphones and the booming digital payments industry in countries like India, China, and Japan, the fingerprint sensor market is primed for unprecedented expansion. In December 2023, the Ministry of Finance, Government of India, announced that the total volume of digital payment transactions in India has surged from USD 252.5 million in 2017-18 to USD 1,643.4 million in 2022-23, registering a remarkable CAGR rate of 45%. The growing digital payment industry is expected to fuel the exponential expansion of the fingerprint sensor market in the region.

Fingerprint Sensor Market by Region

Fingerprint Sensor Market by Region

To know about the assumptions considered for the study, download the pdf brochure

Top Fingerprint Sensor Companies – Key Market Players:

Major vendors in the fingerprint sensor companies include Shenzhen Goodix Technology Co., Ltd. (China), Fingerprints (Sweden), Synaptics Incorporated (US), Apple Inc. (US) NEXT Biometrics (Norway), Novatek Microelectronics Corp. (Taiwan), Qualcomm Technologies, Inc. (US) among others.

1 서론 (페이지 번호 – 28)

1.1 연구 목표

1.2 시장 정의

1.3 연구 범위

1.3.1 대상 시장

1.3.2 지역 범위

1.3.3 고려 된 연도

1.3.4 포함 및 제외 항목

1.4 고려되는 통화

1.5 고려되는 단위

1.6 제한 사항

1.7 이해관계자

1.8 변경 사항 요약

1.9 경기 침체 영향

2 연구 방법론(33페이지)

2.1 연구 접근 방식

2.1.1 2차 데이터

2.1.1.1 주요 2차 자료 목록

2.1.1.2 2차 출처의 주요 데이터

2.1.2 1차 데이터

2.1.2.1 주요 인터뷰 참가자 목록

2.1.2.2 주요 인터뷰 내역

2.1.2.3 주요 출처의 주요 데이터

2.1.2.4 주요 업계 인사이트

2.1.3 2 차 및 1 차 연구

2.2 시장 규모 추정

2.2.1 상향식 접근 방식

2.2.1.1 상향식 분석을 사용한 시장 규모 추정 접근 방식 (수요 측면)

2.2.2 하향식 접근법

2.2.2.1 하향식 분석을 이용한 시장 규모 추정 접근법(공급 측면)

2.3 데이터 삼각측량

2.4 연구 가정

2.5 경기침체가 연구 대상 시장에 미치는 영향을 분석하기 위해 고려되는 매개변수

2.6 위험 평가

2.7 연구 한계

3 실행 요약 (44페이지)

4 프리미엄 인사이트 (페이지 번호 – 48)

4.1 지문 센서 시장의 플레이어를위한 매력적인 기회

4.2 기술 별 지문 센서 시장

4.3 유형 및 센서 기술 별 지문 센서 시장

4.4 최종 용도 애플리케이션 별 지문 센서 시장

4.5 지문 센서 시장, 지역별

4.6 지문 센서 시장, 국가 별

5 시장 개요 (페이지 번호 – 51)

5.1 소개

5.2 시장 역학

5.2.1 동인

5.2.1.1 생체 인증을 위해 소비자 전자 기기에서 지문 센서의 광범위한 사용

5.2.1.2 보안 강화를 위해 법 집행 및 정부 애플리케이션에서 생체 인식의 높은 채택

5.2.1.3 직원 근태 관리 시스템에서 지문 센서 기술 도입 증가

5.2.1.4 신원 도용 및 사기 사건의 증가로 인한 고급 지문 기술에 대한 수요 급증

5.2.1.5 모바일 결제 및 온라인 거래에 대한 선호도 증가

5.2.2 제한 사항

5.2.2.1 생체 인식 데이터와 관련된 보안 위협

5.2.2.2 얼굴 및 홍채 인식과 같은 대체 기술의 가용성

5.2.3 기회

5.2.3.1 은행, 금융 서비스 및 보험 애플리케이션을위한 생체 인식 스마트 카드의 출현

5.2.3.2 생체 인식 솔루션에 IoT의 통합

5.2.3.3 자동차 산업에서 생체 인식 채택 증가

5.2.3.4 3D 지문 기술의 발전

5.2.4 도전 과제

5.2.4.1 지문 센서의 성능 한계

5.3 고객 비즈니스에 영향을 미치는 트렌드 / 중단

5.4 가격 분석

5.4.1 기술별 주요 업체의 평균 판매 가격 추세

5.4.2 지역별 주요 업체의 평균 판매 가격 추세

5.5 가치 사슬 분석

5.6 생태계 분석

5.7 투자 및 자금 조달 시나리오

5.8 기술 분석

5.8.1 주요 기술

5.8.1.1 초음파 지문 인식

5.8.1.2 정전 식 지문 감지

5.8.2 보완 기술

5.8.2.1 생체 인식 융합

5.8.2.2 생동감 감지

5.8.3 인접 기술

5.8.3.1 온 디바이스 머신 러닝

5.9 특허 분석

5.10 무역 분석

5.10.1 데이터 가져오기(HS 코드 847160)

5.10.2 데이터 수출(HS 코드 847160)

5.11 주요 컨퍼런스 및 이벤트, 2024-2025년

5.12 사례 연구 분석

5.12.1 차세대 플래그십 성능을 위해 REALME GT 5G의 엔진을 연료로하는 GOODIX의 지문 및 오디오 솔루션

5.12.2 암호없는 인증을 위해 지문의 생체 인식을 내장 한 보안 FIDO2 보안 키

5.12.3 이지스, 현대에 지문 센서를 공급하여 비밀번호 없이 차량 잠금을 해제하고 개인 설정을 활성화합니다.

5.12.4 내무부(남아프리카공화국)가 주도하는 HANIS 프로젝트를 위해 지문 인식 데이터베이스를 구축하는 NEC 코퍼레이션의 AFIS

5.12.5 향상된 데이터 품질, 보안 및 효율적인 유권자 등록을 제공하여 라이베리아의 2023년 선거를 지원하는 아라텍의 A800 지문 스캐너

5.13 규제 환경

5.13.1 규제 기관, 정부 기관 및 기타 조직

5.13.2 표준 및 규제 정책

5.13.2.1 미국 국립표준기술연구소(NIST) 표준

5.13.2.2 FBI 형사 사법 정보 서비스(CJIS) 보안 정책

5.13.2.3 ISO/IEC 19794

5.13.2.4 ISO/IEC 24745

5.13.2.5 ISO/IEC 17839

5.13.2.6 CE 마크

5.13.2.7 FAP 10

5.13.2.8 FAP 20

5.13.2.9 FAP 30

5.13.2.10 기타

5.13.3 지역/국가별 규정

5.13.3.1 미국

5.13.3.2 유럽

5.13.3.3 중국

5.13.3.4 일본

5.14 포터의 5 가지 힘 분석

5.14.1 경쟁 경쟁의 강도

5.14.2 공급 업체의 협상력

5.14.3 구매자의 협상력

5.14.4 대체품의 위협

5.14.5 신규 진입자의 위협

5.15 주요 이해관계자 및 구매 기준

5.15.1 구매 프로세스의 주요 이해 관계자

5.15.2 구매 기준

6 지문 센서에 사용되는 다양한 재료(84페이지)

6.1 소개

6.2 압전 재료(석영)

6.3 초전 재료(탄탈산 리튬)

6.4 접착제

6.5 코팅 재료

7 지문 센서와 통합된 제품 (페이지 번호 – 86)

7.1 소개

7.2 스마트 기기 및 웨어러블 기기의 인증 시스템

7.3 출석 기록 시스템

7.4 액세스 제어 시스템

7.4.1 생체 인식 시스템

7.4.2 디지털 잠금 장치

7.5 생체 인식 스마트 카드

7.5.1 금융 카드

7.5.2 신분증

7.6 차량

7.7 기타

8 센서 기술별 지문 센서 시장 (페이지 번호 – 89)

8.1 소개

8.2 2D

8.2.1 세그먼트 성장을 촉진하는 2D 센서의 저렴한 비용

8.3 3D

8.3.1 수요를 늘리기 위해 전자 장치의 보안 개선에 대한 관심 증가

9 지문 센서 시장, 유형별 (페이지 번호 – 92)

9.1 소개

9.2 영역 및 터치 센서

9.2.1 면적 및 터치 지문 센서에 대한 수요를 늘리기위한 터치 센서의 기술 발전

9.3 스 와이프 센서

9.3.1 세그먼트 성장을 촉진하기 위해 전자 장치의 보안을 보장해야 함

10 지문 센서 시장, 기술별 (페이지 번호 – 96)

10.1 소개

10.2 용량 성

10.2.1 시장 성장을 촉진하기 위해 모바일 장치에 정전 식 지문 센서의 비용 효율성과 통합 용이성

10.3 광학

10.3.1 스마트 폰 제조업체의 광학 디스플레이 지문 센서 채택 증가로 시장 촉진

10.4 열

10.4.1 생체 인식 스마트 카드에 센서를 사용하여 열 센서 시장의 성장 기회 창출

10.5 초음파

10.5.1 시장을 주도하기 위해 미세한 세부 사항을 캡처하는 초음파 센서의 기능

11 최종 사용 애플리케이션 별 지문 센서 시장 (페이지 번호 – 106)

11.1 소개

11.2 소비자 가전

11.2.1 스마트 폰

11.2.1.1 세그먼트 성장을 촉진하기 위해 스마트 폰에서 지문 인증의 인기 증가

11.2.2 노트북 및 개인용 컴퓨터

11.2.2.1 시장 활성화를위한 보안을 보장하기 위해 랩톱에서 지문 기술 사용 증가

11.2.3 태블릿

11.2.3.1 원격 근무 및 e- 러닝의 증가 추세로 태블릿에 대한 수요 급증으로 부문 별 성장에 기여

11.2.4 웨어러블 기기

11.2.4.1 지문 센서 제공 업체를위한 기회를 창출하기 위해 동적 기능을 갖춘 웨어러블을 제공하려는 선도적 인 OEM의 노력 증가

11.2.5 기타 소비자 전자 제품

11.3 여행 및 출입국 관리

11.3.1 지문 센서에 대한 수요를 늘리기 위해 공항에서 생체 인식 시스템의 급증하는 배포

11.4 정부 및 법 집행 기관

11.4.1 시장 성장을 지원하기 위해 시민들에게 디지털 신원을 제공하기 위한 정부 이니셔티브

11.5 군사, 방위 및 항공 우주

11.5.1 지문 센서에 대한 수요를 높이기 위해 강력한 액세스 제어 시스템에 대한 필요성 증가

11.6 은행 및 금융

11.6.1 부문별 성장을 촉진하기 위해 핀 인증 결제 카드의 대안으로 지문 스캐너 채택

11.7 의료

11.7.1 지문 센서 기반 생체 인식 시스템에 대한 수요를 촉진하기 위해 신원 및 중요한 환자 정보를 보호해야 할 필요성

11.8 스마트 홈

11.8.1 시장 참여자를위한 성장 기회를 창출하기 위해 다양한 OEM에 의한 스마트 잠금 장치 개발

11.9 상업용

11.9.1 성장을 가속화하기 위해 다양한 기업 및 소매점에서 생체 인식 시스템 채택

11.1 기타 최종 사용 애플리케이션

12 지문 센서 시장, 지역별 (페이지 번호 – 144)

12.1 소개

12.2 북미

12.2.1 북미 : 경기 침체 영향

12.2.2 미국

12.2.2.1 플레이어에게 수익성있는 성장 기회를 제공하기 위해 가전 제품 및 은행 및 금융 애플리케이션에서 지문 센서 채택 증가

12.2.3 캐나다

12.2.3.1 시장을 주도하는 이민자 학생 및 근로자 수 증가

12.2.4 멕시코

12.2.4.1 시장 성장을 촉진하기 위해 은행 및 금융, 여행 및 이민 애플리케이션에서 생체 인식 카드 채택 증가

12.3 유럽

12.3.1 유럽 경기 침체 영향

12.3.2 독일

12.3.2.1 시장을 주도하기 위해 지문 기반 차량 내 디지털 결제 서비스의 채택 증가

12.3.3 영국

12.3.3.1 시장 성장을 가속화하기 위해 법 집행 기관에서 지문 기반 생체 인식 솔루션에 대한 수요 증가

12.3.4 프랑스

12.3.4.1 시장 성장에 기여하는 정부 및 법 집행 기관 및 은행 및 금융 애플리케이션

12.3.5 이탈리아

12.3.5.1 시장 성장을 지원하기 위해 공항과 국경에 생체 인식의 신속한 배포

12.3.6 유럽의 나머지 지역

12.4 아시아 태평양

12.4.1 아시아 태평양: 경기 침체 영향

12.4.2 중국

12.4.2.1 시장 성장을 촉진하는 주요 스마트 폰 제조업체의 강력한 입지

12.4.3 일본

12.4.3.1 시장을 주도하기위한 자동차 제조 및 지문 기반 생체 인식 카드의 지배력

12.4.4 인도

12.4.4.1 지문 센서에 대한 수요를 높이기 위해 Aadhaar 이니셔티브에 따라 지문 스캐너 채택 증가

12.4.5 대한민국

12.4.5.1 시장 성장을 가속화하기위한 번성하는 전자 산업

12.4.6 나머지 아시아 태평양 지역

12.5 ROW

12.5.1 ROW: 경기 침체 영향

12.5.2 남미

12.5.2.1 매력적인 성장 기회를 제공하는 은행 및 금융 애플리케이션

12.5.3 중동

12.5.3.1 시장 성장을 지원하기위한 스마트 시티 이니셔티브에 대한 정부의 상당한 투자

12.5.3.2 GCC 국가

12.5.3.3 중동의 나머지 지역

12.5.4 아프리카

12.5.4.1 시장 확장을 지원하기 위해 인터넷 보급률 증가

13 경쟁 환경 (페이지 번호 – 179)

13.1 개요

13.2 주요 업체 전략 / 승리 할 권리, 2021-2024 년

13.3 수익 분석, 2021-2023

13.4 시장 점유율 분석, 2023

13.5 회사 가치 평가 및 재무 지표

13.6 브랜드/제품 비교

13.7 회사 평가 매트릭스 : 주요 업체, 2023 년

13.7.1 별

13.7.2 신흥 리더

13.7.3 퍼베이시브 플레이어

13.7.4 참가자

13.7.5 회사 발자국 : 주요 업체, 2023 년

13.7.5.1 최종 사용 애플리케이션 풋 프린트

13.7.5.2 기술 풋 프린트

13.7.5.3 센서 기술 풋 프린트

13.7.5.4 유형 풋 프린트

13.7.5.5 지역 발자국

13.8 기업 평가 매트릭스: 스타트업/SME, 2023년

13.8.1 진보적 인 기업

13.8.2 반응 형 기업

13.8.3 역동적 인 기업

13.8.4 시작 블록

13.8.5 경쟁 벤치마킹, 스타트 업 / SME, 2023 년

13.8.5.1 주요 스타트 업 / 중소기업의 상세 목록

13.8.5.2 주요 스타트 업 / 중소기업의 경쟁 벤치마킹

13.9 경쟁 시나리오 및 트렌드

13.9.1 제품 출시

13.9.2 거래

14 회사 프로필 (페이지 번호 – 201)

❖본 조사 자료에 관한 문의는 여기를 클릭하세요.❖