❖본 조사 자료의 견적의뢰 / 샘플 / 구입 / 질문 양식❖

이 문서는 열교환기 시장에 대한 포괄적인 분석을 제공합니다. 문서는 여러 섹션으로 나뉘어 있으며, 각 섹션은 시장의 다양한 측면을 다루고 있습니다. 먼저, 소개 부분에서는 열교환기 시장의 중요성과 연구의 목적을 설명합니다. 이어서 연구 방법론이 제시되며, 데이터 수집 및 분석 방법에 대한 설명이 포함됩니다. 임원 요약에서는 연구 결과의 핵심 포인트를 간략하게 정리합니다. 프리미엄 인사이트 섹션에서는 열교환기 시장의 주요 플레이어와 기회, 시장 유형 및 최종 용도 산업별 분석이 이루어집니다. 특히, 국가별 시장 동향도 다루어져 있습니다. 시장 개요 섹션에서는 시장의 역학을 설명하며, 동인, 제한 사항, 기회 및 도전 과제를 분석합니다. 동인으로는 신흥 경제의 산업화, 에너지 효율 규제의 증가, HVAC 및 냉동 장비에 대한 수요 증가 등이 있습니다. 반면, 원자재 가격 변동, 에너지 효율에 대한 인식 부족, 배터리 전기 자동차의 수요 증가 등이 제한 사항으로 언급됩니다. 기회로는 원자력 발전소 수의 증가와 열교환기 애프터 마켓의 성장 가능성이 제시됩니다. 도전 과제로는 불소화 온실가스 관련 규제와 자본 집약적인 시장 구조가 있습니다. 포터의 다섯 가지 힘 분석에서는 대체품의 위협, 공급자의 협상력, 신규 진입자의 위협, 구매자의 협상력 및 경쟁의 강도를 평가합니다. 거시 경제 지표 섹션에서는 글로벌 GDP 동향과 석유 및 가스 통계, 발전 통계가 포함됩니다. 산업 동향 섹션에서는 가치 사슬 분석, 규제 환경, 무역 분석, 가격 분석 및 투자 시나리오를 다룹니다. 특히, 규제 환경에서는 북미, 유럽, 아시아 태평양 지역의 규제와 표준이 설명됩니다. 기술 분석에서는 마이크로 채널 열교환기, 다기능 열교환기, 나노 기술 강화 열교환기 등의 핵심 기술이 소개됩니다. 열교환기 시장은 유형별, 재료별, 최종 사용 산업별로 세분화되어 분석됩니다. 유형별로는 쉘 및 튜브, 플레이트 및 프레임, 공냉식 열교환기 등이 있으며, 각 유형의 시장 동향과 수요 증가 요인이 설명됩니다. 재료별로는 금속, 합금, 브레이징 클래드 재료가 다루어지며, 각 재료의 특성과 시장에서의 역할이 강조됩니다. 마지막으로, 최종 사용 산업별 분석에서는 화학, 에너지, HVAC 및 냉동, 식음료, 전력, 펄프 및 제지 산업에서의 열교환기 사용 현황과 시장 동향이 설명됩니다. 각 산업의 성장 요인과 시장에서의 필요성이 강조되며, 에너지 효율과 환경 규제의 중요성이 부각됩니다. 이 문서는 열교환기 시장의 현재와 미래를 이해하는 데 필요한 다양한 정보를 제공하며, 산업 관계자들에게 유용한 자료가 될 것입니다. |

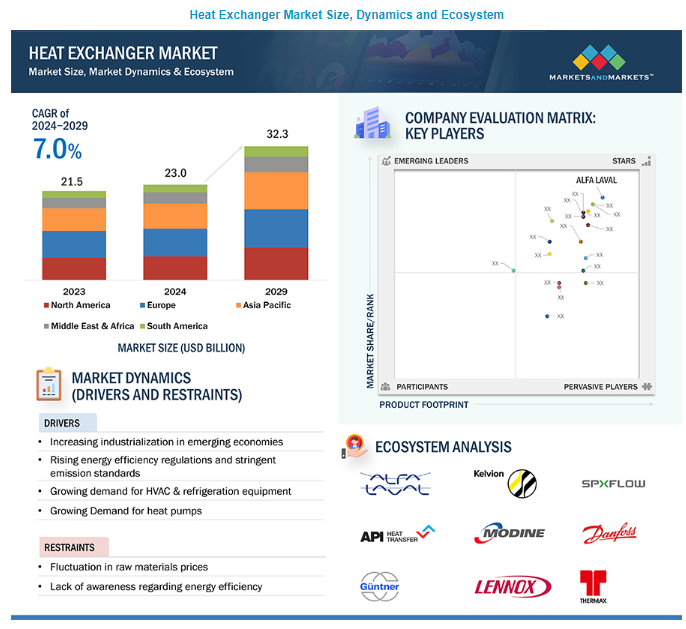

The global heat exchanger market size is projected to reach USD 32.3 billion by 2029 from USD 23.0 billion in 2024, at a CAGR of 7.0% during the forecast period. The heat exchanger market is projected to grow significantly in the coming years. They are an essential part of systems where regulating heat is an important factor. Heat exchangers enable the efficient transfer of heat between fluids, facilitating the effective utilization of energy. The growth in this market is driven by various factors like increasing industrialization in emerging economies, rising energy efficiency regulations and stringent emission standards, growing demand for heat pumps in developed countries due to limitations on conventional heating systems like boilers, and rising demand for sustainable, low-energy consumption & cost-effective heat exchangers. These factors also drive the necessity for research in heat regulation field to find the best solution for sustainability and emission control.

Heat Exchanger Market Size, Dynamics and Ecosystem

Heat Exchanger Market

To know about the assumptions considered for the study, Request for Free Sample Report

Heat Exchanger Market Dynamics

Driver: Growing demand for heat pumps in Europe

Heat exchangers used in heat pumps are essential for transferring heat through mediums such as air, water, or ground. The growing demand for heat pumps in Europe is driving the need for heat exchangers in in these systems. Heat pumps are commonly used in heating systems of residential, commercial, and industrial buildings to provide space heating, hot water, and cooling functionalities. Heat exchangers are used in heat pumps to enable the heat exchange between refrigerant and surrounding environment. Promoting these factors, the European Union are facilitating building renovation to enhance energy efficiency by the adoption of heat pumps. Countries like Poland, Czechia, Italy, France, and Germany are deploying regulations for systematic replacement of traditional heating systems with heat pumps. As older buildings undergo retrofitting with heat pump systems to lower carbon emissions and energy usage, the demand for heat exchangers correspondingly increases.

Restraint: Fluctuations in raw material prices

Heat exchanger manufacturers are always in risk of fluctuating raw material prices. Material like copper, aluminum, steel, and others are facing surge in prices due economic conditions, exchange rates, supply conditions, mining policies, and raw material processing. The Russia Ukraine war has also facilitated the increase in raw material and energy prices in the European region. This volatility in raw material prices impacts the profitability and operational efficiency of heat exchanger manufacturers. The surge in prices leads to unfavorable conditions for customers, which in turn may lead to delays and cancellation of large capital projects. This will directly impact the profitability and integrity of heat exchanger manufacturers. On the other hand, over supply due to reduced cost may impact the competitiveness and market position of heat exchanger manufacturers. These factors will influence the average selling price of heat exchangers in the market.

Opportunity: Growing aftermarket of heat exchangers

Heat exchangers play an important role in process industries, with its performance and durability directly impacting capital and operating expenses. Repair due to breakdown often incur significant costs. Therefore, regular maintenance of heat exchangers is essential for proper functioning of heat exchangers. The maintenance cost of heat exchangers is lower in comparison to equipment such as pumps, fans, and compressors. Regular maintenance of heat exchangers is essential for smooth running of operation, thus, maintaining system uptime, and prevention of sudden failures. Investing in regular maintenance for prevention of system breakdown is often more cost-effective than emergency repairs. Well-planned maintenance of heat exchangers enables companies to save energy and reduce operational costs by up to 30%. Proper maintenance is beneficial in the long run for prevention of pressure drops, which leads to reduced loads on pumps and other components. This will increase heat transfer rates and operational efficiency while maintaining lower energy consumption.

Challenges: Regulations concerning fluorinated gases

Various government agencies and regulatory bodies have highlighted the bad impact of emission of fluorinated gases (F-gases) into the environment. Participants in the supply chain of heat exchangers are often concerned about these regulations. European Union has implemented several regulations and amendments which directly aims at controlling emission of F-gases like hydrofluorocarbons (HFCs) to the environment. These amendments led to the adoption of two legislative acts by the EU. The MAC Directive is implemented for regulating air conditioning systems in small motor vehicles. Similarly, F-gas Regulation are concerned with systems employing the use of F-gases. The regulation lays out conditions for specific uses of fluorinated greenhouse gases and sets numerical thresholds for introducing hydrofluorocarbons into the market. In the US, The American Innovation and Manufacturing Act is a federal law in the United States that requires an 85% decrease in the production of fluorinated gases (F-gases) by 2036. These regulation poses a challenge to the manufacturers. The adaption rate to new regulations will play a crucial role in customer retention and market ranking.

Heat Exchanger Market Segmentation & Geographical Spread

Heat Exchanger Market Segmentation & Geographical Spread

To know about the assumptions considered for the study, download the pdf brochure

By material, metals are the fastest growing in heat exchanger market, in 2023.

Metals, alloys, and brazing clad materials are often used in the manufacturing of heat exchangers. Among these, metal heat exchangers drive the fastest growth in the heat exchanger market. Metals like, copper, aluminum, and stainless steel are excellent thermal conductors. This benefits in the efficient transfer of heat between fluids. This property is essential for rapid heat transfer, thus, making metals highly suitable for use in heat exchangers. Additionally, metal heat exchangers offer good mechanical strength and durability, making them suitable for environments where high temperatures, pressures, mechanical stresses are encountered. Reliability and longevity of heat exchangers is also maintained due to durability of metal heat exchangers. Metal heat exchangers are often cost-effective when compared to other materials.

By type, shell & tube is the largest in heat exchanger market, in 2023.

Shell & tube, plate & frame, and air cooled are some of the major type of heat exchangers. Among these, shell & tube heat exchangers capture the largest market share. The making of these heat exchangers facilitates large surface area between the flowing fluid through tubes and the fluid surrounding the tubes in the shell & tube system. The large surface area is essential for effective heat transfer among the fluids. This build up increases the heat transfer efficiency and allows shell & tube heat exchangers to be used in various applications. These heat exchangers also have high mechanical strength and are resistant to corrosion. These factors make shell & tube heat exchangers reliable to the customers, even when subjected to challenging operating conditions.

By end-use industry, energy segment is the second fastest growing end-use industry in the heat exchanger market, in 2023.

Heat exchangers are essential components in various end-use industries like, chemicals, energy, HVAC & refrigeration, food & beverages, power generation, pulp & paper, and other end-use industries. Energy system captures the second largest share for the use of heat exchanger. Heat exchanger is used in energy systems for efficient heat transfer to control temperatures, generate electricity, provide heating and cooling, and facilitate energy conversion processes. They are also used heat regulation in renewable energy systems like solar thermal collectors, geothermal heat pumps, and biomass boilers. These systems harness renewable energy sources to generate heat for space heating, hot water production, and industrial processes.

Asia Pacific accounted for the second largest market share in the heat exchanger market, in terms of value.

Based on region, Asia Pacific is a key market to produce heat exchangers and is projected to grow at a CAGR of 8.3% in terms of value during the forecasted period. The availability of low-cost raw materials and labor, coupled with increasing domestic demand, makes the region an attractive investment destination for cooling towers manufacturers. The rising population, urbanization, industrialization, and growing concerns related to infrastructure development in China and India are some of the factors that will drive the cooling tower market in this region. The leniency of regulations also drives the manufacturing market of heat exchangers in Asia Pacific.

Heat Exchanger Market Players

Some of the key players operating in the heat exchanger market include ALFA LAVAL (Sweden), Kelvion Holding GmbH (Germany), Danfoss (Denmark), Exchanger Industries Limited (Canada), Mersen (France), API Heat Transfer (US), Boyd (US), H. Güntner (UK) Limited (Germany), Johnson Controls (Ireland), Xylem (US), Wabtec Corporation (US), SPX FLOW (US), LU-VE S.p.A. (Italy), Lennox International Inc. (US), and Modine Manufacturing Company (US) among others.

These companies have adopted various organic as well as inorganic growth strategies between 2019 and 2023 to strengthen their positions in the market. The new product launch is the key growth strategy adopted by these leading players to enhance regional presence and develop product portfolios to meet the growing demand for heat exchangerfrom emerging economies.

Read More: Heat Exchangers Companies

Heat Exchanger Market Report Scope

Report Metric

Details

Years considered for the study

2020-2029

Base Year

2023

Forecast period

2024–2029

Units considered

Units; Value (USD Million)

Segments

Material, Type, End-Use Industry, and Region

Regions

Asia Pacific, North America, Europe, Middle East & Africa, and South America

Companies

ALFA LAVAL (Sweden), Kelvion Holding GmbH (Germany), Danfoss (Denmark), Exchanger Industries Limited (Canada), Mersen (France), API Heat Transfer (US), Boyd (US), H. Güntner (UK) Limited (Germany), Johnson Controls (Ireland), Xylem (US), Wabtec Corporation (US), SPX FLOW (US), LU-VE S.p.A. (Italy), Lennox International Inc. (US), and Modine Manufacturing Company (US).

This report categorizes the global heat exchangers market based on material, type, end-use industry, and region.

Based on the material:

Metals

Steel

Carbon Steel

Stainless Steel

Copper

Aluminum

Titanium

Nickel

Other Metals

Alloys

Nickel Alloys

Hastelloy

Inconel

Monel

Other Nickel Alloys

Copper Alloys

Titanium Alloys

Other Alloys

Brazing Clad Materials

Copper Brazing

Ni Clad Brazing

Phosphor Copper Brazing

Silver Brazing

Other Brazing Clad Materials

Based on the type:

Shell & Tube

Plate & Frame

Air Cooled

Other Types

Based on the end-use industry:

Chemical

Energy

HVACR

Food & Beverage

Power Generation

Pulp & Paper

Other End-Use Industries

Based on the region:

Asia Pacific

Europe

North America

South America

Middle East & Africa

Recent Developments

In December 2023, ALFA LAVAL partnered with Outokumpu, a global steel manufacturer, to reduce carbon emissions by utilizing Outokumpu’s Circle Green stainless steel in the production of Alfa Laval’s heat exchangers. This partnership targets a decrease in the carbon footprint associated with Alfa Laval’s heat exchangers, which typically consist of up to 80 percent stainless steel, by transitioning from conventional stainless steel to a material with a significantly reduced carbon footprint, amounting to half of its original level.

In November 2023, Danfoss Heat Exchangers signed an agreement with Danfoss Commercial Compressors to establish an in-house test capability for propane located in the ATEX-certified lab in Trevoux in France. The new propane test facility focuses on testing brazed plate heat exchangers ranging from 10 to 150kW capacity.

In September 2023, Kelvion Holding GmbH has invested USD 4.3 million to expand its production capacities in Sarstedt to meet the increasing demand for its heat exchangers across diverse end-use sectors. This expansion enables the facility to manufacture an extra 150,000 heat exchangers annually, aligning with the company’s strategic goal of expanding its presence in the U.S. market and establishing itself as the preferred partner in the Refrigeration and Data Center Industries.

1 소개

2 연구 방법론

3 임원 요약

4 프리미엄 인사이트 (페이지 번호 – 46)

4.1 열교환 기 시장 플레이어를위한 매력적인 기회

4.2 유형별 열교환 기 시장

4.3 최종 용도 산업별 열교환 기 시장

4.4 열교환 기 시장, 국가 별

5 시장 개요 (페이지 번호 – 48)

5.1 소개

5.2 시장 역학

5.2.1 동인

5.2.1.1 신흥 경제의 산업화 증가

5.2.1.2 에너지 효율 규제 및 엄격한 배출 기준 증가

5.2.1.3 HVAC 및 냉동 장비에 대한 수요 증가

5.2.1.4 열 펌프에 대한 수요 증가

5.2.1.5 지속 가능하고 에너지 소비가 적으며 비용 효율적인 열교환기에 대한 수요 증가

5.2.2 제한 사항

5.2.2.1 원자재 가격 변동

5.2.2.2 에너지 효율에 대한 인식 부족

5.2.2.3 배터리 전기 자동차에 대한 수요 증가

5.2.2.4 부진한 성장률

5.2.3 기회

5.2.3.1 원자력 발전소 수 증가

5.2.3.2 열교환 기 애프터 마켓 성장

5.2.4 도전 과제

5.2.4.1 불소화 온실 가스 관련 규제

5.2.4.2 자본 집약적 인 시장

5.3 포터의 다섯 가지 힘 분석

5.3.1 대체품의 위협

5.3.2 공급 업체의 협상력

5.3.3 신규 진입자의 위협

5.3.4 구매자의 협상력

5.3.5 경쟁 경쟁의 강도

5.4 거시 경제 지표

5.4.1 글로벌 GDP 동향

5.4.2 석유 및 가스 통계

5.4.3 발전 통계

6 산업 동향 (페이지 번호 – 61)

6.1 소개

6.2 가치 사슬 분석

6.2.1 원자재 소싱

6.2.2 제조

6.2.3 유통

6.2.4 최종 사용자

6.3 규제 환경

6.3.1 규제

6.3.1.1 북미

6.3.1.2 유럽

6.3.1.3 아시아 태평양

6.3.2 표준

6.3.2.1 ISO 27.060.30

6.3.2.2 BS EN 308:2022

6.3.2.3 ASME 보일러 및 압력 용기 코드(BPVC)

6.3.2.4 TEMA(관형 교환기 제조업체 협회) 표준

6.3.2.5 API(미국석유협회) 표준

6.3.2.6 PD500 표준

6.3.2.7 EN 13445 표준

6.3.3 규제 기관, 정부 기관 및 기타 조직

6.4 무역 분석

6.4.1 HS 코드

6.4.2 수입 시나리오

6.4.3 수출 시나리오

6.5 가격 분석

6.5.1 지역별 평균 판매 가격 추세

6.5.2 유형별 평균 판매 가격

6.5.3 최종 용도 산업별 주요 업체의 평균 판매 가격 추세

6.6 투자 및 자금 조달 시나리오

6.7 생태계/시장 지도

6.8 고객의 비즈니스에 영향을 미치는 트렌드 / 중단

6.9 기술 분석

6.9.1 핵심 기술

6.9.1.1 마이크로 채널 열교환 기

6.9.1.2 다기능 열교환 기

6.9.1.3 나노 기술 강화 열교환 기

6.9.2 보완 기술

6.9.2.1 3D 프린팅 열교환 기

6.9.2.2 소형 및 마이크로 홈 열교환 기

6.10 사례 연구 분석

6.10.1 API 열전달

6.10.2 BOYD

6.10.3 API 열전달

6.11 주요 컨퍼런스 및 이벤트, 2024-2025년

6.12 특허 분석

6.12.1 방법론

6.12.2 특허 유형

6.12.3 지난 10 년 동안의 출판 동향

6.12.4 인사이트

6.12.5 특허의 법적 지위

6.12.6 관할권 분석

6.12.7 상위 신청자

6.13 주요 이해 관계자 및 구매 기준

6.13.1 구매 프로세스의 주요 이해 관계자

6.13.2 구매 기준

6.14 애플리케이션 별 자금 조달

7 열교환 기 시장, 유형별 (페이지 번호 – 84)

7.1 소개

7.2 쉘 및 튜브 열교환 기

7.2.1 시장을 주도하기 위해 다양한 최종 사용 산업의 수요 증가

7.2.2 관형 열교환 기

7.2.3 고정 튜브 열교환 기

7.2.4 U- 튜브 열교환 기

7.2.5 플로팅 헤드 열교환기

7.3 플레이트 및 프레임 열교환 기

7.3.1 시장을 주도하는 비용 효율성과 내구성

7.3.2 개스킷 플레이트 및 프레임 열교환 기

7.3.3 용접 플레이트 및 프레임 열교환 기

7.3.4 브레이징 열교환 기

7.4 공냉식 열교환 기

7.4.1 시장을 주도하기 위해 화학 및 에너지 산업에서 사용 증가

7.4.2 강제 통풍 열교환 기

7.4.3 유도 통풍 열교환 기

7.5 기타 유형

7.5.1 확장 된 표면 열교환 기

7.5.2 재생 열교환 기

8 열교환 기 시장, 재료 별 (페이지 번호 – 92)

8.1 소개

8.1.1 금속

8.1.1.1 시장을 주도하는 높은 열전도율과 내구성

8.1.1.2 강철

8.1.1.2.1 탄소강

8.1.1.2.2 스테인리스 스틸

8.1.1.3 구리

8.1.1.4 알루미늄

8.1.1.5 티타늄

8.1.1.6 니켈

8.1.1.7 기타 금속

8.1.2 합금

8.1.2.1 시장을 주도하는 극도의 환경 친화적 인 특성

8.1.2.2 니켈 합금

8.1.2.2.1 하 스텔로이 합금

8.1.2.2.2 인코넬 합금

8.1.2.2.3 모넬 합금

8.1.2.2.4 기타 니켈 합금

8.1.2.3 구리 합금

8.1.2.4 티타늄 합금

8.1.2.5 기타 합금

8.1.3 브레이징 클래드 재료

8.1.3.1 시장 추진을위한 내식성 및 열전도도 향상

8.1.3.2 구리 브레이징

8.1.3.3 Ni 클래드 브레이징

8.1.3.4 인광체 구리 브레이징

8.1.3.5은 브레이징

8.1.3.6 기타 브레이징 클래드 재료

9 열교환기 시장, 최종 사용 산업별 (페이지 번호 – 100)

9.1 소개

9.2 화학

9.2.1 시장을 주도하기 위해 화학 산업에서 광범위한 사용

9.2.2 기본 화학 물질

9.2.3 중간 화학 물질

9.2.4 특수 화학 물질

9.3 에너지

9.3.1 시장을 주도하기 위해 열 회수에 대한 사용 증가

9.3.2 석유 화학 제품

9.3.3 석유 및 가스

9.4 HVAC 및 냉동

9.4.1 인구 증가, 도시화 및 소득 증가로 시장 주도

9.4.2 지역 난방 및 냉방

9.4.3 상업용 냉동

9.4.4 에어컨

9.4.5 산업용 냉동

9.5 식음료

9.5.1 시장을 주도하기위한 에너지 효율 및 엄격한 환경 규제의 필요성

9.5.2 가공 식품

9.5.3 유제품

9.5.4 설탕 및 에탄올 생산

9.5.5 기타 식음료

9.6 전력

9.6.1 시장 추진을위한 열 관리 개선

9.6.2 재생 가능

9.6.3 비 재생 가능

9.7 펄프 및 제지

9.7.1 연료 소비 감소 및 시장 추진을위한 운영 비용 절감

9.8 기타 최종 사용 산업

9.8.1 야금

9.8.2 폐수 처리

9.8.3 광업

10 열교환 기 시장, 지역별 (페이지 번호 – 109)

10.1 소개

10.2 북미

10.2.1 경기 침체 영향

10.2.2 미국

10.2.2.1 시장을 주도하기위한 DOE의 효율성 표준 변경

10.2.3 캐나다

10.2.3.1 시장 성장에 기여할 수있는 방대한 천연 자원의 가용성

10.2.4 멕시코

10.2.4.1 발전 수요를 주도하는 인구 증가

10.3 유럽

10.3.1 경기 침체 영향

10.3.2 독일

10.3.2.1 시장을 주도하기위한 에너지 전환

10.3.3 프랑스

10.3.3.1 시장 성장에 영향을 미치는 탄소 중립 이니셔티브

10.3.4 영국

10.3.4.1 시장 활성화를위한 지속 가능하고 에너지 효율적인 난방 솔루션

10.3.5 이탈리아

10.3.5.1 시장을 주도하기위한 지속 가능성의 필요성

10.3.6 러시아

10.3.6.1 열교환기에 대한 수요를 늘리기위한 석유 및 가스 부문

10.3.7 터키

10.3.7.1 수요 증대를위한 도시화 및 생활 수준 향상

10.3.8 유럽의 나머지 지역

10.4 아시아 태평양

10.4.1 경기 침체 영향

10.4.2 중국

10.4.2.1 시장 성장을위한 급속한 산업화와 번성하는 최종 사용 산업

10.4.3 일본

10.4.3.1 시장을 주도하는 식음료, 건설 및 원자력 산업

10.4.4 인도

10.4.4.1 수요 증대를위한 에너지 및 발전 최종 사용 산업의 급속한 산업화

10.4.5 대한민국

10.4.5.1 시장 부양을위한 상업용 건설 증가

10.4.6 나머지 아시아 태평양 지역

10.5 남미

10.5.1 경기 침체 영향

10.5.2 브라질

10.5.2.1 시장에 영향을 미치는 자연 재해로 인한 에너지 전환

10.5.3 아르헨티나

10.5.3.1 수요를 늘리기 위해 비 수력 재생 가능 자원에 집중

10.5.4 남미의 나머지 지역

10.6 중동 및 아프리카

10.6.1 경기 침체의 영향

10.6.2 GCC 국가

10.6.2.1 사우디 아라비아

10.6.2.1.1 시장을 주도하는 상업용 건설 및 HVAC 산업 증가

10.6.2.2 카타르

10.6.2.2.1 열교환 기 수요 증가에 기여하는 석유 및 가스 산업

10.6.2.3 기타 GCC 국가

10.6.2.3.1 시장을 주도하기위한 지역 냉각 시스템 채택

10.6.3 중동 및 아프리카의 나머지 지역

11 경쟁 환경 (페이지 번호 – 212)

11.1 개요

11.2 주요 업체 전략

11.3 수익 분석, 2021-2023

11.4 시장 점유율 분석, 2023 년

11.4.1 시장 순위 분석

11.5 회사 가치 평가 및 재무 지표

11.6 브랜드 / 제품 비교

11.7 회사 평가 매트릭스 : 주요 업체, 2023 년

11.7.1 별

11.7.2 신흥 리더

11.7.3 퍼베이시브 플레이어

11.7.4 참가자

11.7.5 회사 발자국

11.7.5.1 회사 유형 발자국

11.7.5.2 회사 재료 발자국

11.7.5.3 회사 최종 사용 산업 발자국

11.7.5.4 회사 지역 발자국

11.7.5.5 회사 전체 발자국

11.8 기업 평가 매트릭스 : 스타트 업 및 SMES, 2023 년

11.8.1 진보적 인 기업

11.8.2 반응 형 기업

11.8.3 역동적 인 기업

11.8.4 시작 블록

11.8.5 경쟁 벤치마킹

11.9 경쟁 시나리오 및 트렌드

11.9.1 제품 출시

11.9.2 거래

11.9.3 확장

12 회사 프로필(240페이지)

❖본 조사 자료에 관한 문의는 여기를 클릭하세요.❖